Retire Confidently from Phillips 66

We specialize in oil and gas retirement planning and help P66 employees:

✔️ Design tax-efficient retirement income

✔️ Make informed decisions about your 401(k), pension, and RSUs

✔️ Coordinate healthcare, estate, and tax planning

Introduction

As a Phillips 66 employee, you have access to a wide range of financial and retirement benefits but understanding how they fit together along with how to optimize them can be challenging.

This guide breaks down each major benefit, how they work, and how you can strategically use them to reduce taxes, build wealth, and plan confidently for retirement.

Section 1: Compensation Overview

Compensation Structure

Phillips 66 compensation is built on three pillars:

- Base Salary

- Variable Cash Incentive Program (VCIP)

- Equity Compensation (RSUs)

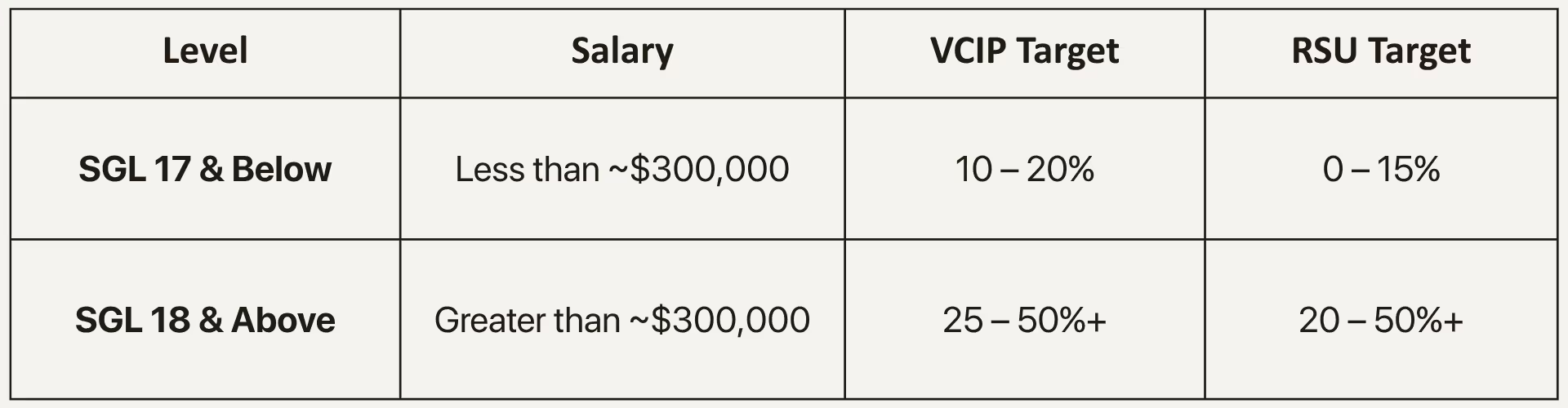

Subject to change with new grading systems in 2025–2026.

Additional benefits for executives SGL 21+.

For our more detailed table by SGL please send me an email or book a Free Assessment call to discuss.

Section 2: Core Retirement Benefits

401(k) Savings Plan at Vanguard

The Phillips 66 401(k) is among the strongest corporate retirement plans in the energy industry.

Key Highlights

- Company Match:

Phillips 66 matches 100% of your contributions up to 8% of salary — invested each paycheck.

You must contribute at least 8% per pay period to capture the full match. - Contribution Limits (2025):

- Employee deferrals: $23,500

- Catch-up (age 50+): +$7,500

- IRS pay limit: $355,000

- While 401(k) contributions stop once you reach the IRS compensation limit, Phillips 66 allows eligible employees, typically those expected to exceed this limit I.e. SGL 18+ to also participate in the company’s Deferred Compensation Plans (see below).

- Investment Options:

- A variety of low cost index, active and target date funds.

- For more information on how to decide on a strategy, see:

- 🎥 The 5 Levels of 401(k) Investing (From Beginner to Advanced)

- Because this makes up a large portion of most employees net worth, we offer hourly consultations to design the right investment mix for your goals. Book a Free Assessment to learn more.

The Mega Backdoor Roth 401(k)

A powerful but often overlooked feature within the Phillips 66 plan is the Mega Backdoor Roth.

You make after-tax 401(k) contributions and convert them in-plan to Roth. Converted amounts grow and be withdrawn tax-free in retirement if Roth distribution requirements are satisfied.

However, you must elect this conversion on the Vanguard site. If you do not convert, earnings on after-tax contributions will accrue tax-deferred and will be taxable upon distribution.

Section 3: Pension Benefits

Phillips 66 Cash Balance Account

Most active employees today participate in the Cash Balance Pension Plan, a hybrid defined-benefit plan offering predictable, company-funded growth.

How It Works

- Pay Credits: Each month, Phillips 66 credits a % of your eligible pay to your “Cash Balance Account.”

- Interest Credits: The balance grows annually at a company-defined rate, typically tied to Treasury yields.

- Vesting: Fully vested after 3 years of service.

- Distribution Options:

- Lifetime annuity payments

- Lump-sum rollover to an IRA or qualified plan

Heritage Pension Plans

Employees prior to 2002 may still participate in a Heritage Pension Plan with unique formulas and early-retirement eligibility rules.

- Phillips Retirement Income Plan

- Retirement Plan of Conoco (COP)

- Tosco Pension Plan

- Burlington Resources Pension Plan

- Burlington Resources Cash Balance Plan

Check your personalized benefit statement or HR portal to confirm which plan applies to you.

Section 4: Executive & Key Employee Plans (SGL 18+)

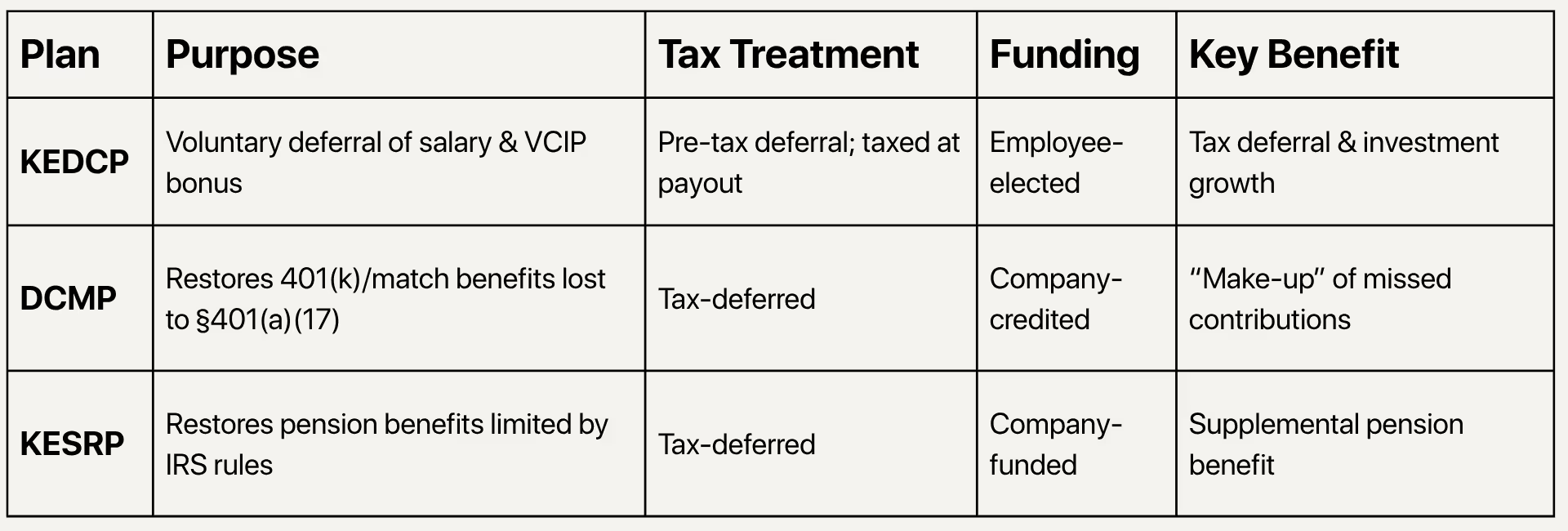

For Key Employees (SGL 18 and above), Phillips 66 offers three powerful non-qualified plans designed to supplement savings beyond IRS limits.

- Phillips 66 Key Employee Deferred Compensation Plan (KEDCP):

- This voluntary deferred compensation plan provides tax-efficient retirement savings by allowing executives to voluntarily defer both the receipt and taxation of a portion of their base salary and annual bonus until a specified date or when they leave the Company.

- At Phillips 66, employees can defer the following:

- Salary: 0–50% of base salary

- VCIP: 0–100% of annual bonus

- Participating in the KEDCP reduces your taxable income (and, therefore, your tax bill) in the year the income is deferred. This can be invested and grow tax-free until it's distributed back to you according to the distribution schedule you elect during your enrollment window (see below).

- At distribution, the income is taxed as ordinary income.

- Phillips 66 Defined Contribution Make-Up Plan (DCMP):

- This defined contribution restoration plan restores benefits capped under the qualified defined contribution plan due to Internal Revenue Code (IRC) limits. To “make up” for this lost benefit, Phillips 66 credits that excess compensation to a non-qualified plan like the Defined Contribution Make-Up Plan (DCMP) or the KEDCP.

- Phillips 66 Key Employee Supplemental Retirement Plan (KESRP):

- This defined benefit restoration plan restores Company-sponsored benefits capped under the qualified defined benefit pension plan due to IRC limits.

So the KEDCP is how you “defer your compensation” (NQDC), DCMP is “make up the match / thrift / savings benefits you lose by hitting caps,” and KESRP is “make up pension benefits you lose by hitting caps.”

- After Separation from Service: Participants can choose from flexible payout options, determined when the deferral is made:

- 1–15 annual installments

- 2–30 semiannual installments

- 4–60 quarterly installments

- Timing: The first payment must begin at least one year after separation and no later than five years after separation (to comply with IRC §409A). Alternatively, participants may choose a date-certain payout while still employed (subject to similar timing rules).

- Default: If no election is made, payment is typically a lump sum beginning six months after separation.

Executive Employees (SGL 21+): Stock option program (since stopped), performance shares, sign on bonuses (inducement grants), increased life insurance can all also apply at the higher levels.

Executives can also receive an Executive Health Program and Executive Financial Counseling. Although the company covers the cost, the value is taxable. Example: a $10,000 benefit taxed at a 35% marginal rate results in roughly $3,500 of tax.

Section 5: RSUs (Restricted Stock Units)

How RSUs Work

- Vesting:

- SGL 17 and below — ⅓ each year over 3 years

- SGL 18+ — Cliff vest after 3 years

- Taxation:

- Ordinary income upon vesting (based on stock price at that time)

- Capital gains or losses only apply on future price changes post-vesting

Planning Opportunities

- Use RSU income to:

- Maximize 401(k) or Mega Roth contributions

- Fund charitable giving strategies

- Offset tax impact with deferred comp elections (KEDCP)

Section 6: Integrating Your Benefits

When strategically layered, Phillips 66’s plans allow high-income employees to save multiple six figures annually in tax-advantaged vehicles.

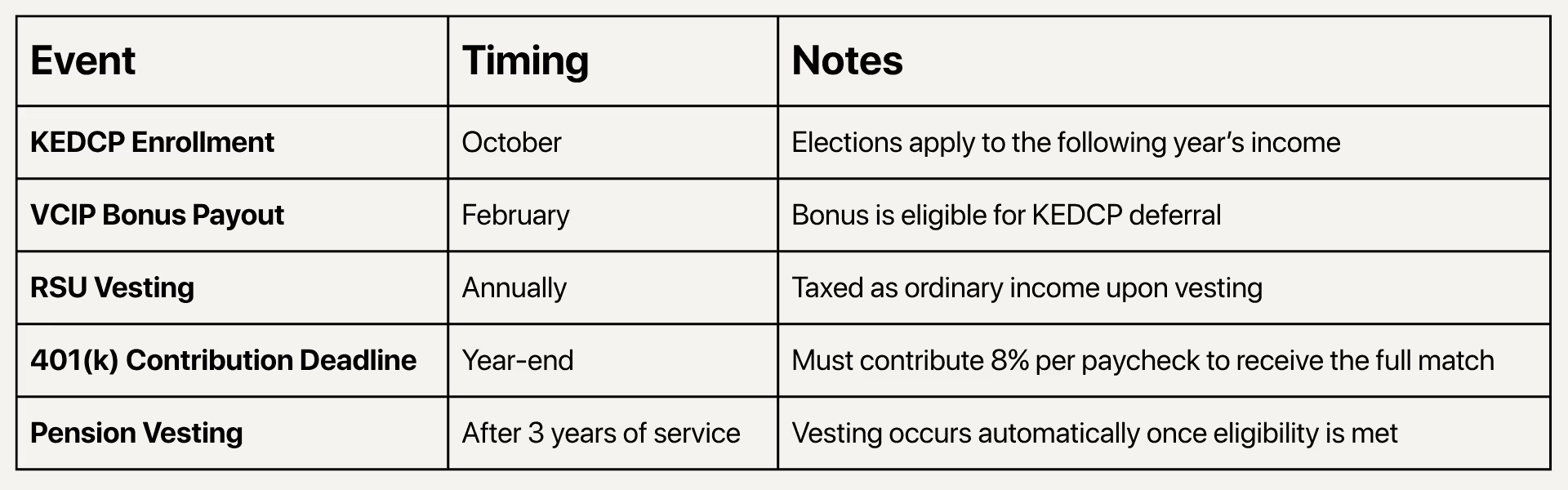

Section 7: Important Dates & Deadlines

Section 8: Planning Considerations

Before Enrolling in KEDCP, Ask Yourself:

- What is my current vs. projected future tax rate?

- How much should I defer to balance current cash flow with tax benefits?

- What payout schedule best fits my retirement income needs?

- How will this interact with other income sources (RSUs, pension, or 401(k))?

Top Mistakes to Avoid:

- Missing the October KEDCP enrollment deadline

- Overlooking the §401(a)(17) compensation cap (losing match potential)

- Ignoring RSU vesting tax implications

- Electing a pension lump sum without coordinating rollover and tax strategies

Phillips 66 offers one of the strongest total compensation and benefits packages in the energy industry. If you have questions or would like to learn more about how we help Phillips 66 employees optimize their benefits and plan for retirement, please don’t hesitate to reach out.

This guide is for educational purposes only and is not affiliated with or endorsed by Phillips 66. Information is based on sources believed to be reliable but may change without notice. Employees should consult official Phillips 66 plan documents or HR for the most current details. Refined Wealth is a fee-only fiduciary advisory firm and does not represent Phillips 66.

Joe Ward, CFP®, RICP®

I know how complex retirement in oil and gas can be. At Refined Wealth, I help Phillips 66 professionals retire with clarity, confidence, and a plan built for them.

Work With Joe